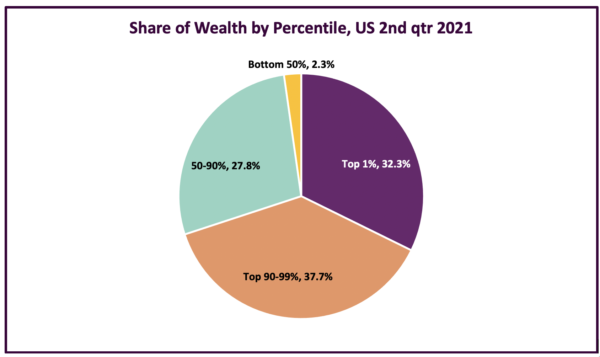

The COVID pandemic has disproportionately harmed the health and economic security of Black and Brown workers and households, while the wealth of billionaires in the U.S. has soared by 70% since March 2020. According to Federal Reserve data, for the first time the top 1% of Americans hold more wealth than the entire 60% of middle-income households.

The concentration of wealth at the top and the racial wealth gap are national problems with particular expressions in Washington State. The litany of murders of Black people by police across the United States and in Washington cities, coupled with the COVID public health and economic crises, have made it abundantly clear — we need to change policies at every level of government and work together to rebuild a new Washington rooted in equity. This begins by acknowledging the root causes of racial inequity.

Increasing Concentration of Wealth at the Top

The concentration of wealth in the hands of a small elite has made weathering the pandemic harder for all moderate- and lower-income households, but particularly for Black, Indigenous, and other People of Color families who have faced both historical and continuing obstacles to wealth-building. Wealth includes the total value of assets such as homes, stocks and bonds, pensions, businesses, and savings, minus debts. Having individual or family assets makes it much easier for people to pursue higher education, buy a home, or start a business without taking on crippling debt. Wealth builds a foundation of intergenerational economic stability, and when monthly income gets disrupted or extra expenses pop up, wealth makes it much easier to get through without a family financial crisis.

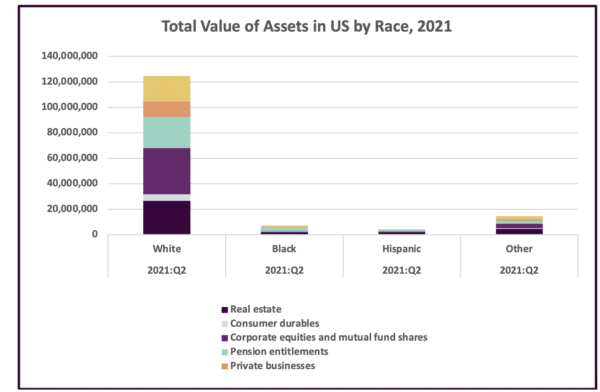

Over the past 30 years, the share of total national wealth held by the top 1% in the U.S. has grown steadily, while the share owned by the bottom 90% has shrunk. The top 10% now hold 70% of all wealth in the country. White Americans hold nearly 83% of this wealth, while making up just 60% of the U.S. population.

Sources: Board of Governors of the Federal Reserve System, Wealth by Wealth Percentile Group, Oct. 1, 2021

Great wealth also confers power and the ability to influence public policy. Despite the popularity with voters of issues such as paid family leave, child care investments, affordable health care, and reining in prescription drug prices, Congress has been slow to act. President Biden’s Build Back Better plan originally incorporated these and other policies that would help counter the trend toward ever greater inequality, and make economic security achievable for the vast majority of working and retired Americans of all races. The proposal pays for enhanced services by raising tax rates on sources of income of the super-rich to be on par with rates paid by working people on their earnings. But the Build Back Better proposal faces intense opposition from special interests, and political pressure to scale back. As of this writing, it remains stalled in Congress.

Continuing Racial Discrimination in Home Ownership – the Cornerstone of Middle-Class Wealth

For the majority of Americans, home ownership is a major component of personal and family wealth. Across the U.S., a 20% to 30% gap between Black and white homeownership rates has persisted for more than 100 years. Redlining, restrictive housing covenants, and other overtly racist practices during the 20th century prevented Black and other racial and ethnic groups from living in or purchasing homes in many neighborhoods. Even now, banks and other mortgage providers persist in giving white applicants far more favorable terms than Black applicants. As a result, Black homeowners pay higher rates of interest than white homeowners with the same or even lower incomes. Higher rates of interest mean higher monthly payments, slower accumulation of equity, and a greater likelihood of losing the home during an economic crisis. Black homeowners also face discrimination by appraisers who assign lower values to houses of Black residents than to similar houses of white neighbors.

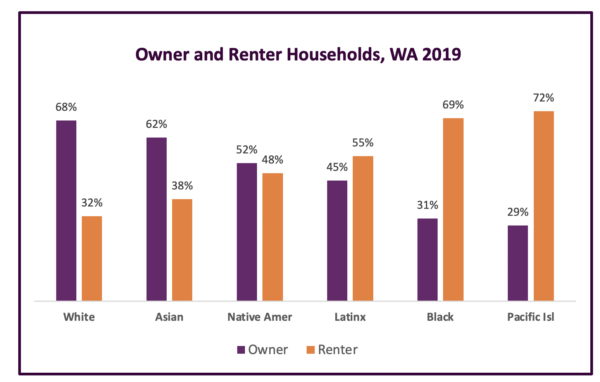

These same patterns play out in Washington State, where BIPOC households are much more likely to rent their homes than white households.

U.S. Census Bureau; American Community Survey, 2019 American Community Survey 1-Year Estimates, Table S2502

A recent report from Prosperity Now explores the racial wealth divide in the Seattle area. It describes the local history of redlining and racially restrictive covenants, and the current trends of gentrification and rising housing costs that are resulting in displacement in historically BIPOC communities. White Seattle residents today are more likely to own rather than rent their home than Asian, Latinx, Black, or Native American residents.

Financial Wealth

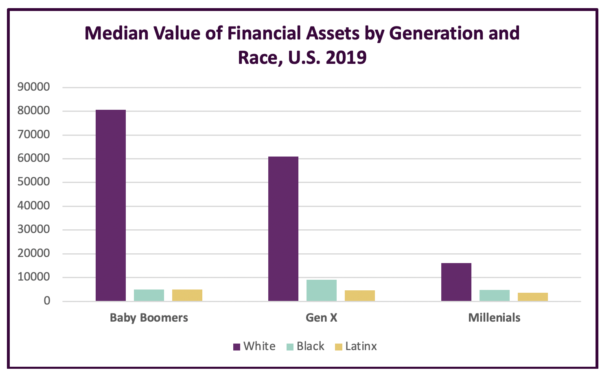

Financial assets are particularly inequitably distributed across race and class. To the extent that households in the middle 40th to 80th percentile hold assets such as stocks, bonds, and mutual funds, they are largely in retirement accounts. But the balance shifts higher up the economic ladder, according to Federal Reserve data, with most of that wealth outside retirement accounts for the top 1%. Analysis of financial wealth by the National Institute on Retirement Security across generation, race, and class found that because of deep inequality, even the majority of Baby Boomers — currently aged 75 to 57 — are unprepared for a secure retirement. The median, or typical, value of financial assets for Black and Latinx members of the Baby Boom, Gen X, and Millennial generations is less than $10,000. The median value of financial assets held by white Baby Boomers and Gen X members is considerably higher at $80,100 and $61,000, respectively. Those assets can help tide a family over if a job is lost or help a child go to college, but these levels do not assure much of a supplement to Social Security income over potentially two to three decades of retirement.

Source: National Institute On Retirement Security, Stark Inequality: Financial Assets Inequality Undermines Retirement Security, Aug 2021

These wealth disparities interact with and amplify disparities and discrimination in other institutions such as our schools, employment, incarceration system, and health care

Quality K-12 and higher education are major factors in achieving economic security and opportunity. Children of Color in Washington are more likely to attend under-resourced and underfunded K-12 schools, and to be disciplined more frequently and harshly than white children for similar behavior. They are also less likely to access higher education and complete a degree.

COVID-19 has highlighted the concentration of Black and Brown people in frontline, low-wage, and volatile occupations that we now consider “essential.” Decades after enactment of equal employment laws, repeated studies document continued racial discrimination in the job market. For instance, recent research out of Harvard documents how white workers are given much more favorable shifts with more stable and higher earnings than workers of Color in the same company with the same education level. In Washington, Black workers make approximately 60 cents for every dollar paid to a white worker, according to 2019 American Community Survey data.

Washington’s incarceration rate more than doubled between 1978 and 2016. Black and Brown people make up a disproportionate share of the prison population. The war on drugs, the state’s “three strikes” law, aggressive policing of Black and Brown communities, and harsher sentences all play a role. Families and communities suffer financially, as well as emotionally, when a loved one is behind bars. A conviction can haunt a person for life, making it harder to secure housing, land a job, or receive financial aid for college.

The disproportionate impact of COVID-19 on Black and Brown people highlights the cumulative impact of economic disparities, racist systems, and policy choices. While making up just 6% of King County’s total population, African Americans account for 13% of COVID-19 cases. Rates of infant and maternal death and chronic diseases such as asthma are also much higher for Black and Brown residents.

Explicitly racist policies and ongoing institutional racism have barred most Black and Brown families from accumulating even modest amounts of wealth. While many of these policies are no longer in place, families continue to suffer from their impacts. “Color-blind” policies, such as “three strikes” laws, and the burden of legal financial obligations, along with continuing biases and stereotypes in schools, the workplace, banks, and law enforcement perpetuate racially disparate outcomes. As a result, Black and Brown families own a fraction of white wealth across all levels of income and educational attainment. We cannot successfully advance educational opportunity, good jobs, healthy families and workplaces, and a dignified retirement for all without tackling these legacies directly.

Designing policies thoughtfully to promote equitable access and avoid perpetuating harm to Black and Brown communities will benefit everybody and make economic opportunity a reality for all. For example, recent state legislation and emerging proposals to make higher education more affordable have included funding for counseling, child care, and other student supports. Research has shown that such services are critically important to help BIPOC students complete degrees, but they help the majority of white students, too.

To repair the damage of systemic racism and come out stronger from the current economic crisis, we will need to make significant investments in the most impacted communities in ways that build community power and acknowledge past harm.

More To Read

May 19, 2025

A year of reflections, a path forward

Read EOI Executive Director's 2025 Changemaker Dinner speech

March 24, 2025

Remembering former Washington State House Speaker Frank Chopp

Rep. Chopp was Washington state’s longest-serving Speaker of the House

February 11, 2025

The rising cost of health care is unsustainable and out of control

We have solutions that put people over profits